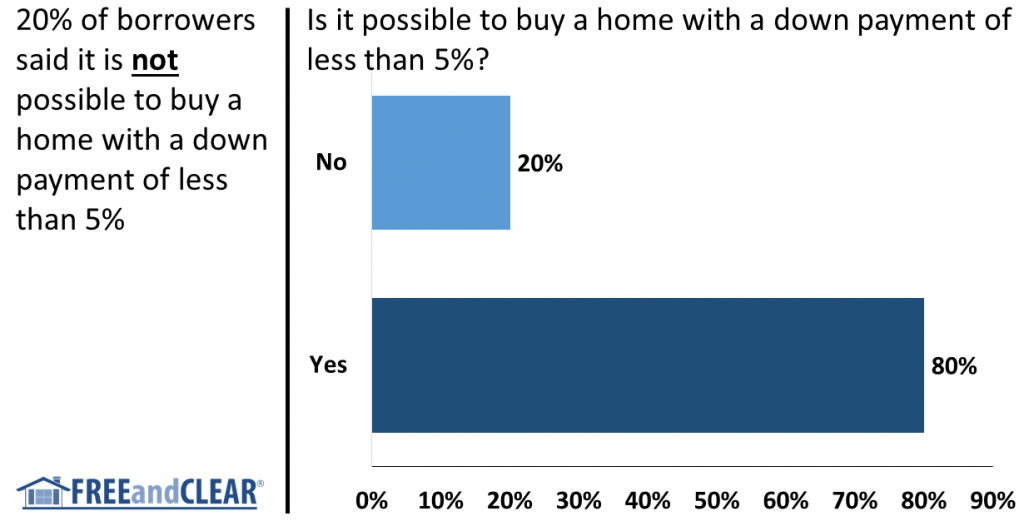

The only thing worse than not knowing something is thinking you know something when you really do not. When it comes to mortgage borrowers, the bad news is that most borrowers are not knowledgeable about mortgages. The good news is that most borrowers recognize they are not knowledgeable about mortgages.

According to the FREEandCLEAR Mortgage Survey, approximately 60% of borrowers rated themselves a six or lower when asked how knowledgeable they are about mortgages, on a scale of one to ten, with ten being the most knowledgeable. So six out of ten borrowers gave themselves a grade of D or below when asked to assess how much they know about mortgages. Getting a mortgage to buy a house is one of the largest financial commitments most people make and the survey results demonstrate that borrowers are painfully uninformed about mortgages, but at least they admit it.

Borrowers are not very knowledgeable about mortgages

Our mortgage survey also asked borrowers a series of follow-up question to evaluate their self-assessment. We were hoping that these questions would demonstrate that borrowers know more about mortgages then they think and they were grading themselves too critically. It turns out that borrowers assessed themselves relatively honestly as many borrowers lack knowledge about mortgage fundamentals.

For example, we asked borrowers for what type of mortgage can the monthly payment change — fixed rate mortgage, interest only mortgage and adjustable rate mortgage — and select all that apply. 18% of borrowers said that the mortgage payment on a fixed rate mortgage can change over the course of the loan while only 20% of borrowers said the payment can change on an interest only mortgage. The monthly payment on a fixed rate mortgage never changes while the payment on an interest only mortgage can fluctuate and increase over the life of the loan. These results reflect borrowers’ lack of understand of how different mortgage programs work. On a more positive note, 84% of survey respondents correctly answered that the monthly payment on an adjustable rate mortgage is subject to change, although the 16% of respondents who got this question wrong certainly raises a red flag.

Many borrowers do not understand how mortgage programs work

We also asked borrowers to select the length of mortgage you pay the least amount of interest on over the life of the mortgage — 10 year, 15 year, 20 year or 30 year mortgage. 28% of borrowers answered this question incorrectly with 9% of borrowers selecting a 30 year mortgage, which requires borrowers to pay the most amount of interest over the life of the loan. While 72% of respondents selected the correct answer — 10 year mortgage — the results of this questions demonstrate that many borrowers do not understand mortgage basics including how your mortgage term impacts how much interest you pay over the course of your loan.

Many borrowers did not select the length of mortgage that requires the least interest expense

Our mortgage survey is designed to highlight important issues such as borrower knowledge. This latest batch of survey results reinforce how much work needs to be done to ensure that borrowers are informed when they get a mortgage. Educating borrowers is a significant challenge that requires participation from all members of the real estate, mortgage and education communities, and especially the involvement of borrowers. The good news is that most borrowers realize they need it.